Fail to replicate ISDA Fair Value CDS Model

|

This post was updated on .

Hi,

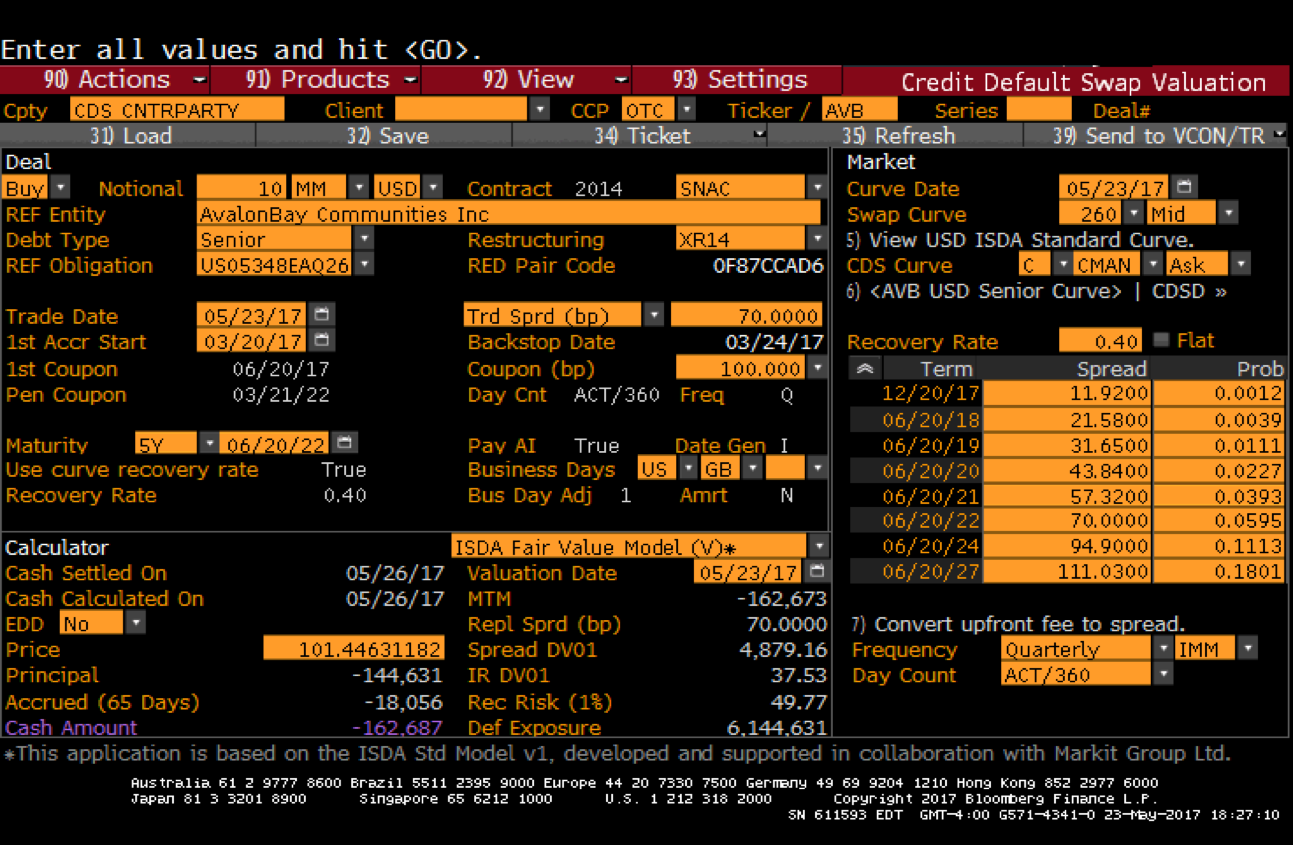

I'm really new to quantlib so please pardon me for any stupid questions. I have built Quantlib using the SWIG bindings for Python and tried to use it to replicate the ISDA Fair Value CDS pricing engine (i.e. using real yield curve and spread curve and assuming piecewise constant harzard rate). I modified Luigi's sample code on GitHub and created the sample code below. It seems that the hazard curve generated from the code is very different from the Bloomberg result (see screenshot below). Any ideas why this happens? Thanks in advance... Alan Modified Code: CDS.py Bloomberg Screenshot:  |

Re: Fail to replicate ISDA Fair Value CDS Model

|

|

May you post the code as an attachment? For some reason, its lines got all mashed together, which made it unreadable. Luigi On Fri, May 26, 2017 at 12:19 AM wwd1015 <[hidden email]> wrote: Hi, I'm really new to quantlib so please pardon me for any stupid questions. I have built Quantlib using the SWIG bindings for Python and tried to use it to replicate the ISDA Fair Value CDS pricing engine (i.e. using real yield curve and spread curve and assuming piecewise constant harzard rate). I modified Luigi's sample code on GitHub and created the sample code below. It seems that the hazard curve generated from the code is very different from the Bloomberg result (see screenshot below). Any ideas why this happens? Thanks in advance... Alan from QuantLib import * calendar = TARGET() # Set evaluation date todaysDate = Date(23, 5, 2017); todaysDate = calendar.adjust(todaysDate) # business day adjustment Settings.instance().evaluationDate = todaysDate # CDS parameters recovery_rate = 0.4 quoted_spreads = [0.001192, 0.002158, 0.003165, 0.004384, 0.005732, 0.007000, 0.009490, 0.011103] tenors = [Period(6, Months), Period(1, Years), Period(2, Years), Period(3, Years), Period(4, Years), Period(5, Years), Period(7, Years), Period(10, Years)] maturities = [calendar.adjust(todaysDate + x, Following) for x in tenors] spotRates = [0.010294, 0.010989, 0.011920, 0.014193, 0.017265, 0.015215, 0.016575, 0.017645, 0.018625, 0.019415, 0.020185, 0.020830, 0.021310, 0.021855, 0.022705, 0.023460, 0.024160, 0.024335, 0.024440] spotPeriod = [Period(1, Months), Period(2, Months), Period(3, Months), Period(6, Months), Period(1, Years), Period(2, Years), Period(3, Years), Period(4, Years), Period(5, Years), Period(6, Years), Period(7, Years), Period(8, Years), Period(9, Years), Period(10, Years), Period(12, Years), Period(15, Years), Period(20, Years), Period(25, Years), Period(30, Years)] spotDates = [todaysDate + x for x in spotPeriod] risk_free_rate = YieldTermStructureHandle( ZeroCurve(spotDates, spotRates, Actual360()) ) # CDS instruments instruments = [ SpreadCdsHelper(QuoteHandle(SimpleQuote(s)), tenor, 0, calendar, Quarterly, Following, DateGeneration.TwentiethIMM, Actual360(), recovery_rate, risk_free_rate) for s, tenor in zip(quoted_spreads, tenors)] hazard_curve = PiecewiseFlatHazardRate(todaysDate, instruments, Actual360()) print("Calibrated hazard rate values: ") for x in hazard_curve.nodes(): print("hazard rate on %s is %.7f" % x) # reprice instruments nominal = 1000000.0 probability = DefaultProbabilityTermStructureHandle(hazard_curve) # create a cds for every maturity all_cds = [] for maturity, s in zip(maturities, quoted_spreads): schedule = Schedule(todaysDate, maturity, Period(Quarterly), calendar, Following, Following, DateGeneration.TwentiethIMM, False) cds = CreditDefaultSwap(Protection.Seller, nominal, s, schedule, Following, Actual360()) engine = MidPointCdsEngine(probability, recovery_rate, risk_free_rate) cds.setPricingEngine(engine) all_cds.append(cds) print("Repricing of quoted CDSs employed for calibration: ") for i in range(len(tenors)): print("%s fair spread: %.7g" % (tenors[i], all_cds[i].fairSpread())) print(" NPV: %g" % all_cds[i].NPV()) print(" default leg: %.7g" % all_cds[i].defaultLegNPV()) print(" coupon leg: %.7g" % all_cds[i].couponLegNPV()) ------------------------------------------------------------------------------ Check out the vibrant tech community on one of the world's most engaging tech sites, Slashdot.org! http://sdm.link/slashdot _______________________________________________ QuantLib-users mailing list [hidden email] https://lists.sourceforge.net/lists/listinfo/quantlib-users |

|

|

Thanks for the reply, Luigi. I have attached the modified code as the attachment.

Alan |

Re: Fail to replicate ISDA Fair Value CDS Model

|

|

Hello Alan, as far as I can see, you're using the available classes correctly, but the existing mid-point engine doesn't implement the ISDA model exactly. We have a pull request for that (https://github.com/lballabio/QuantLib/pull/112) which for some reason has not yet been merged on the master branch. You can try checking the PR out and using it, but you'll have to export the new classes to Python. Luigi On Tue, May 30, 2017 at 4:12 AM wwd1015 <[hidden email]> wrote: Thanks for the reply, Luigi. I have attached the modified code as the ------------------------------------------------------------------------------ Check out the vibrant tech community on one of the world's most engaging tech sites, Slashdot.org! http://sdm.link/slashdot _______________________________________________ QuantLib-users mailing list [hidden email] https://lists.sourceforge.net/lists/listinfo/quantlib-users |

«

Return to quantlib-users

|

1 view|%1 views

| Free forum by Nabble | Edit this page |