Dear,

I'm having a Root not bracketed error when trying to bootstrap a CDS structure.

// Bootstrap hazard rates

boost::shared_ptr<PiecewiseDefaultCurve<HazardRate, BackwardFlat> >

hazardRateStructure(

new PiecewiseDefaultCurve<HazardRate, BackwardFlat>(

todaysDate,

instruments,

dayCounter

));

The error is:

1st iteration: failed at 23rd alive instrument, pillar September 30th, 2051, maturity September 30th, 2051, reference date September 30th, 2028: root

not bracketed: f[2.22045e-016,1] -> [-1.314319e-006,-9.924420e-003]

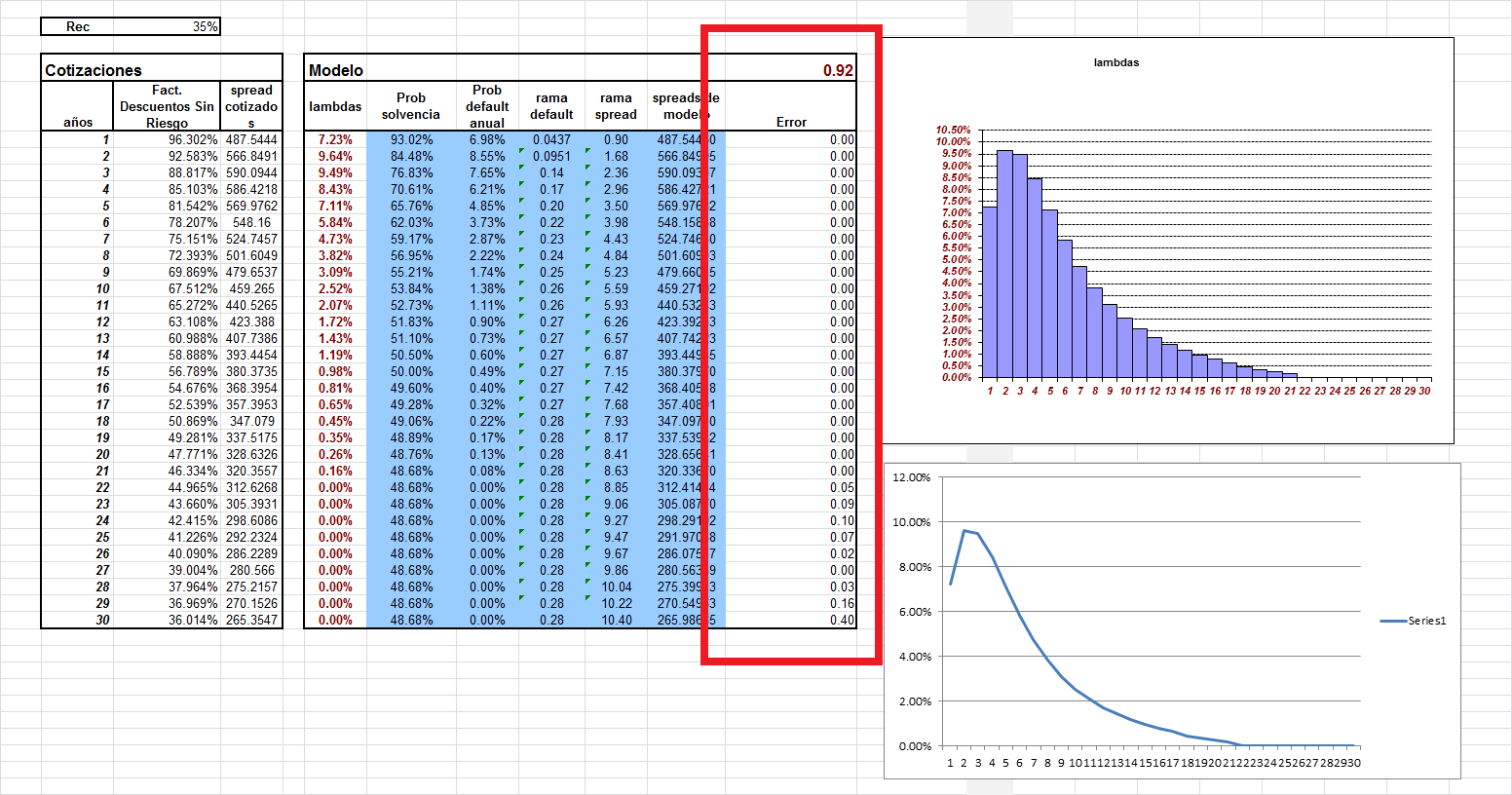

I have made the BackWardFlat bootstrapping in excel with certain tolerance in the mean square error. (0.92)

Not sure about how to deal with this on Quantlib. I'm trying to give some tolerance to my PiecewiseDefaultCurve method but with no luck.

boost::shared_ptr<PiecewiseDefaultCurve<HazardRate, BackwardFlat> >

hazardRateStructure(

new PiecewiseDefaultCurve<HazardRate, BackwardFlat>(

todaysDate,

instruments,

dayCounter,

0.1 <-

));

Would you please have any suggestion?

Many thanks in advance,

Best regards

------------------------------------------------------------------------------

Find and fix application performance issues faster with Applications Manager

Applications Manager provides deep performance insights into multiple tiers of

your business applications. It resolves application problems quickly and

reduces your MTTR. Get your free trial!

https://ad.doubleclick.net/ddm/clk/302982198;130105516;z_______________________________________________

QuantLib-users mailing list

[hidden email]

https://lists.sourceforge.net/lists/listinfo/quantlib-users