Fail to replicate ISDA Fair Value CDS Model

Posted by wwd1015 on

URL: http://quantlib.414.s1.nabble.com/Fail-to-replicate-ISDA-Fair-Value-CDS-Model-tp18310.html

Hi,

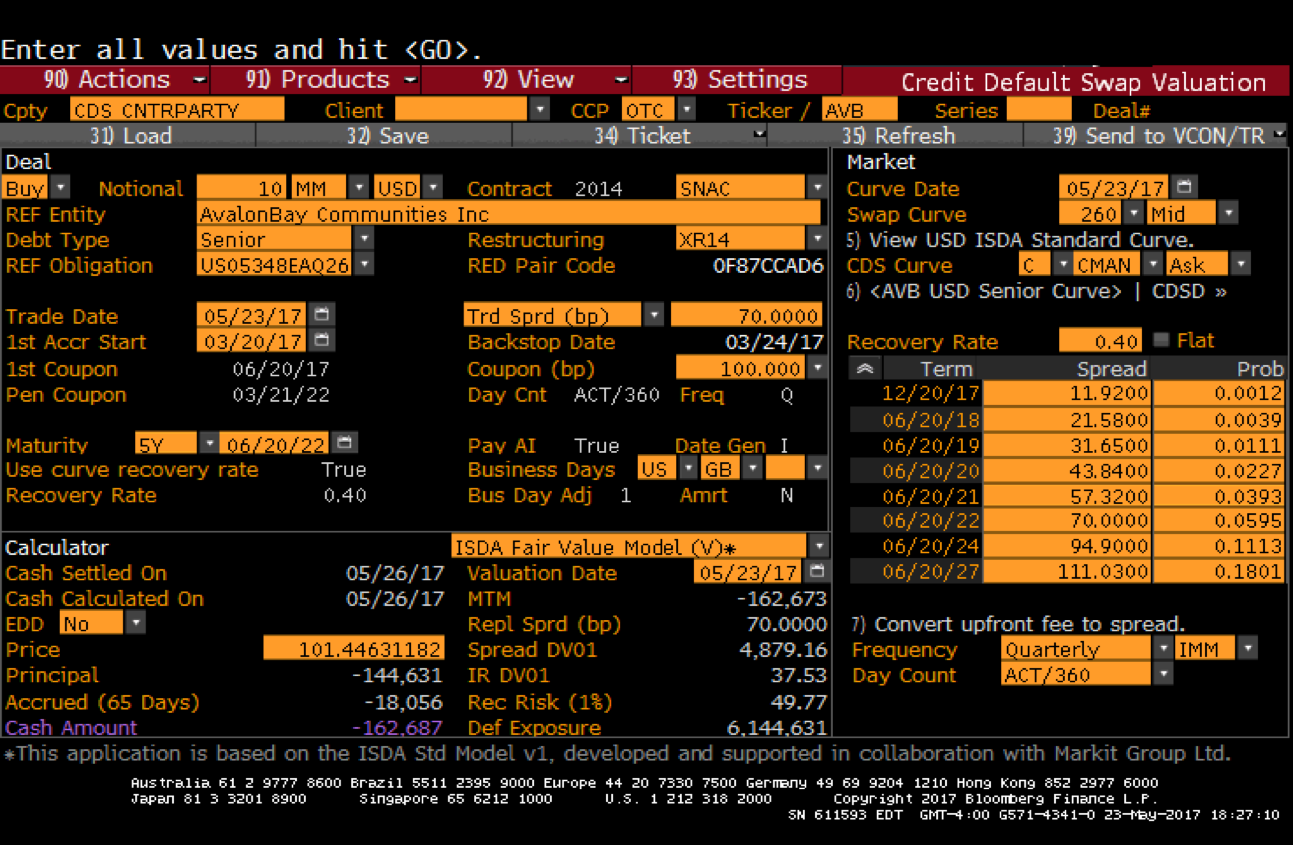

I'm really new to quantlib so please pardon me for any stupid questions. I have built Quantlib using the SWIG bindings for Python and tried to use it to replicate the ISDA Fair Value CDS pricing engine (i.e. using real yield curve and spread curve and assuming piecewise constant harzard rate). I modified Luigi's sample code on GitHub and created the sample code below. It seems that the hazard curve generated from the code is very different from the Bloomberg result (see screenshot below). Any ideas why this happens?

Thanks in advance...

Alan

Modified Code:

CDS.py

Bloomberg Screenshot:

URL: http://quantlib.414.s1.nabble.com/Fail-to-replicate-ISDA-Fair-Value-CDS-Model-tp18310.html

Hi,

I'm really new to quantlib so please pardon me for any stupid questions. I have built Quantlib using the SWIG bindings for Python and tried to use it to replicate the ISDA Fair Value CDS pricing engine (i.e. using real yield curve and spread curve and assuming piecewise constant harzard rate). I modified Luigi's sample code on GitHub and created the sample code below. It seems that the hazard curve generated from the code is very different from the Bloomberg result (see screenshot below). Any ideas why this happens?

Thanks in advance...

Alan

Modified Code:

CDS.py

Bloomberg Screenshot:

| Free forum by Nabble | Edit this page |