Smooth Forward Curve from Market Rates

Posted by newbie730 on

URL: http://quantlib.414.s1.nabble.com/Smooth-Forward-Curve-from-Market-Rates-tp640.html

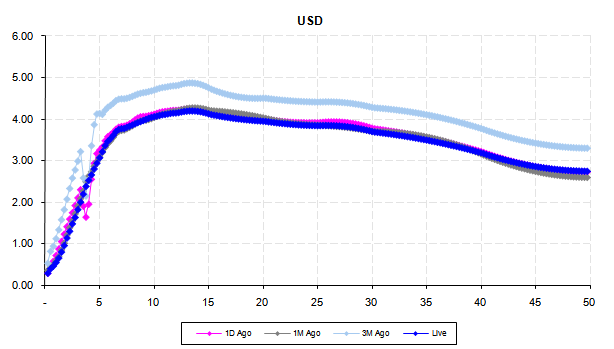

I have attached a screenshot of the 3 month forwards implied by current market quotes using the Piecewise Bootstrapped Term Structure - the resulting curve, as you can see, is not smooth at all. Is it possible to get the market implied forwards with a smooth interpolation?

Note the smooth-usd.png file - is something like this possible using QuantLib and actual market rates?

Further - notice the tail end of the two curves, the QL term structure is implying forwards of > 3.5% past the 40 year point where the actual market forwards are just under 3%. This is clearly inaccurate if one were to trade a long-dated forward swap.

URL: http://quantlib.414.s1.nabble.com/Smooth-Forward-Curve-from-Market-Rates-tp640.html

I have attached a screenshot of the 3 month forwards implied by current market quotes using the Piecewise Bootstrapped Term Structure - the resulting curve, as you can see, is not smooth at all. Is it possible to get the market implied forwards with a smooth interpolation?

Note the smooth-usd.png file - is something like this possible using QuantLib and actual market rates?

Further - notice the tail end of the two curves, the QL term structure is implying forwards of > 3.5% past the 40 year point where the actual market forwards are just under 3%. This is clearly inaccurate if one were to trade a long-dated forward swap.

| Free forum by Nabble | Edit this page |