Shocking the Zero Curve

Posted by rob.philipp on

URL: http://quantlib.414.s1.nabble.com/Shocking-the-Zero-Curve-tp9655.html

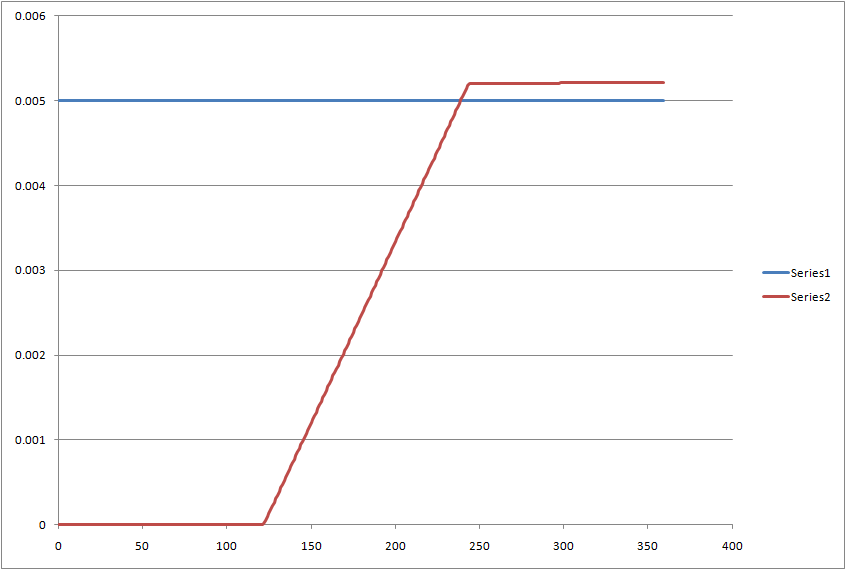

The PiecewiseZeroSpreadedTermStructure class does not shock correctly when the compounding is different from continuous. In particular, if you shock the zero curve (compounded, annual for example) by 50 bps and then take the difference between the base and the shocked zero curves, the difference is not 50 bps as you would expect. Instead the difference ranges from about 50 bps to 52 bps.

I believe that the way forward rates are shocked is incorrect. In the code, the spread (shock) is simply added to the forward curve of the base. The forward curve should be based on the shocked zero curve instead. Has anyone fixed that? If not, I'll try to fix that as well.

Not sure how best to contribute the code. Is there a staging area for checking in the code?

I marked the areas changed, and commented out code from the base version. Following code (QuanlLib-1.0) is also attached:

/* -*- mode: c++; tab-width: 4; indent-tabs-mode: nil; c-basic-offset: 4 -*- */

/*

Copyright (C) 2006 Roland Lichters

Copyright (C) 2006, 2008 StatPro Italia srl

This file is part of QuantLib, a free-software/open-source library

for financial quantitative analysts and developers - http://quantlib.org/

QuantLib is free software: you can redistribute it and/or modify it

under the terms of the QuantLib license. You should have received a

copy of the license along with this program; if not, please email

[hidden email]. The license is also available online at

<http://quantlib.org/license.shtml>.

This program is distributed in the hope that it will be useful, but WITHOUT

ANY WARRANTY; without even the implied warranty of MERCHANTABILITY or FITNESS

FOR A PARTICULAR PURPOSE. See the license for more details.

*/

/*! \file piecewisezerospreadedtermstructure.hpp

\brief Piecewise-zero-spreaded term structure

*/

#ifndef quantlib_piecewise_zero_spreaded_term_structure_hpp

#define quantlib_piecewise_zero_spreaded_term_structure_hpp

#include <ql/termstructures/yield/zeroyieldstructure.hpp>

#include <ql/quote.hpp>

#include <vector>

namespace QuantLib {

//! Term structure with an added vector of spreads on the zero-yield rate

/*! The zero-yield spread at any given date is linearly interpolated

between the input data.

\note This term structure will remain linked to the original

structure, i.e., any changes in the latter will be

reflected in this structure as well.

\ingroup yieldtermstructures

*/

class PiecewiseZeroSpreadedTermStructure : public ZeroYieldStructure {

public:

PiecewiseZeroSpreadedTermStructure(

const Handle<YieldTermStructure>&,

const std::vector<Handle<Quote> >& spreads,

const std::vector<Date>& dates,

// added (RP, 2010.08.23)

Compounding comp = Continuous,

Frequency freq = NoFrequency,

const DayCounter& dc = DayCounter());

//! \name YieldTermStructure interface

//@{

DayCounter dayCounter() const;

Natural settlementDays() const;

Calendar calendar() const;

const Date& referenceDate() const;

Date maxDate() const;

//@}

protected:

//! returns the spreaded zero yield rate

Rate zeroYieldImpl(Time) const;

// added (RP, 20100823)

//! returns the spreaded forward rate

Rate forwardImpl(Time) const;

void update();

private:

void updateTimes();

const double calcSpread( Time t ) const;

Handle<YieldTermStructure> originalCurve_;

std::vector<Handle<Quote> > spreads_;

std::vector<Date> dates_;

std::vector<Time> times_;

// added (RP, 2010.08.23)

Compounding comp_;

Frequency freq_;

DayCounter dc_;

};

// inline definitions

inline

PiecewiseZeroSpreadedTermStructure::PiecewiseZeroSpreadedTermStructure(

const Handle<YieldTermStructure>& h,

const std::vector<Handle<Quote> >& spreads,

const std::vector<Date>& dates,

// added (RP, 2010.08.23)

Compounding comp,

Frequency freq,

const DayCounter& dc)

: originalCurve_(h), spreads_(spreads), dates_(dates),

times_(dates_.size()),

// added (RP, 2010.08.23)

comp_(comp), freq_(freq), dc_(dc) {

QL_REQUIRE(!spreads_.empty(), "no spreads given");

QL_REQUIRE(spreads_.size() == dates_.size(),

"spread and date vector have different sizes");

registerWith(originalCurve_);

for (Size i = 0; i < spreads_.size(); i++)

registerWith(spreads_[i]);

updateTimes();

}

inline DayCounter PiecewiseZeroSpreadedTermStructure::dayCounter() const {

return originalCurve_->dayCounter();

}

inline Calendar PiecewiseZeroSpreadedTermStructure::calendar() const {

return originalCurve_->calendar();

}

inline Natural PiecewiseZeroSpreadedTermStructure::settlementDays() const {

return originalCurve_->settlementDays();

}

inline const Date&

PiecewiseZeroSpreadedTermStructure::referenceDate() const {

return originalCurve_->referenceDate();

}

inline Date PiecewiseZeroSpreadedTermStructure::maxDate() const {

return std::min(originalCurve_->maxDate(), dates_.back());

}

inline Rate

PiecewiseZeroSpreadedTermStructure::zeroYieldImpl(Time t) const {

//Rate z = originalCurve_->zeroRate(t, Continuous, NoFrequency, true);

//if (t <= times_.front()) {

// return z + spreads_.front()->value();

//} else if (t >= times_.back()) {

// return z + spreads_.back()->value();

//} else {

// Size i;

// for (i = 0; i < times_.size(); i++)

// if (times_[i] > t) break;

// Time dt = times_[i] - times_[i-1];

// return z + spreads_[i]->value() * (t - times_[i-1]) / dt

// + spreads_[i-1]->value() * (times_[i] - t) / dt;

//}

// added (RP, 20100823)

double spread = calcSpread( t );

InterestRate zeroRate = originalCurve_->zeroRate(t, comp_, freq_, true);

InterestRate spreadedRate(zeroRate + spread,

zeroRate.dayCounter(),

zeroRate.compounding(),

zeroRate.frequency());

return spreadedRate.equivalentRate(Continuous, NoFrequency, t);

}

inline const double

PiecewiseZeroSpreadedTermStructure::calcSpread( Time t ) const {

double spread = 0.0;

if (t <= times_.front()) {

spread = spreads_.front()->value();

} else if (t >= times_.back()) {

spread = spreads_.back()->value();

} else {

Size i;

for (i = 0; i < times_.size(); i++)

if (times_[i] > t) break;

Time dt = times_[i] - times_[i-1];

spread = spreads_[i]->value() * (t - times_[i-1]) / dt

+ spreads_[i-1]->value() * (times_[i] - t) / dt;

}

return spread;

}

inline void PiecewiseZeroSpreadedTermStructure::update() {

updateTimes();

ZeroYieldStructure::update();

}

inline void PiecewiseZeroSpreadedTermStructure::updateTimes() {

for (Size i = 0; i < dates_.size(); i++)

times_[i] = timeFromReference(dates_[i]);

}

}

#endif

50 bps Key Rate Shock (before):

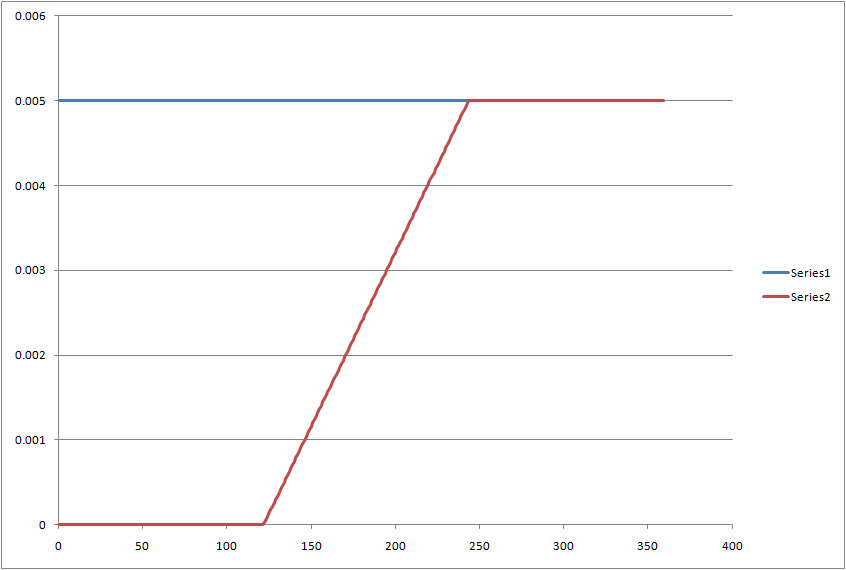

50 bps Key Rate Shock (after fix):

------------------------------------------------------------------------------

Sell apps to millions through the Intel(R) Atom(Tm) Developer Program

Be part of this innovative community and reach millions of netbook users

worldwide. Take advantage of special opportunities to increase revenue and

speed time-to-market. Join now, and jumpstart your future.

http://p.sf.net/sfu/intel-atom-d2d

_______________________________________________

QuantLib-dev mailing list

[hidden email]

https://lists.sourceforge.net/lists/listinfo/quantlib-dev

URL: http://quantlib.414.s1.nabble.com/Shocking-the-Zero-Curve-tp9655.html

The PiecewiseZeroSpreadedTermStructure class does not shock correctly when the compounding is different from continuous. In particular, if you shock the zero curve (compounded, annual for example) by 50 bps and then take the difference between the base and the shocked zero curves, the difference is not 50 bps as you would expect. Instead the difference ranges from about 50 bps to 52 bps.

I believe that the way forward rates are shocked is incorrect. In the code, the spread (shock) is simply added to the forward curve of the base. The forward curve should be based on the shocked zero curve instead. Has anyone fixed that? If not, I'll try to fix that as well.

Not sure how best to contribute the code. Is there a staging area for checking in the code?

I marked the areas changed, and commented out code from the base version. Following code (QuanlLib-1.0) is also attached:

/* -*- mode: c++; tab-width: 4; indent-tabs-mode: nil; c-basic-offset: 4 -*- */

/*

Copyright (C) 2006 Roland Lichters

Copyright (C) 2006, 2008 StatPro Italia srl

This file is part of QuantLib, a free-software/open-source library

for financial quantitative analysts and developers - http://quantlib.org/

QuantLib is free software: you can redistribute it and/or modify it

under the terms of the QuantLib license. You should have received a

copy of the license along with this program; if not, please email

[hidden email]. The license is also available online at

<http://quantlib.org/license.shtml>.

This program is distributed in the hope that it will be useful, but WITHOUT

ANY WARRANTY; without even the implied warranty of MERCHANTABILITY or FITNESS

FOR A PARTICULAR PURPOSE. See the license for more details.

*/

/*! \file piecewisezerospreadedtermstructure.hpp

\brief Piecewise-zero-spreaded term structure

*/

#ifndef quantlib_piecewise_zero_spreaded_term_structure_hpp

#define quantlib_piecewise_zero_spreaded_term_structure_hpp

#include <ql/termstructures/yield/zeroyieldstructure.hpp>

#include <ql/quote.hpp>

#include <vector>

namespace QuantLib {

//! Term structure with an added vector of spreads on the zero-yield rate

/*! The zero-yield spread at any given date is linearly interpolated

between the input data.

\note This term structure will remain linked to the original

structure, i.e., any changes in the latter will be

reflected in this structure as well.

\ingroup yieldtermstructures

*/

class PiecewiseZeroSpreadedTermStructure : public ZeroYieldStructure {

public:

PiecewiseZeroSpreadedTermStructure(

const Handle<YieldTermStructure>&,

const std::vector<Handle<Quote> >& spreads,

const std::vector<Date>& dates,

// added (RP, 2010.08.23)

Compounding comp = Continuous,

Frequency freq = NoFrequency,

const DayCounter& dc = DayCounter());

//! \name YieldTermStructure interface

//@{

DayCounter dayCounter() const;

Natural settlementDays() const;

Calendar calendar() const;

const Date& referenceDate() const;

Date maxDate() const;

//@}

protected:

//! returns the spreaded zero yield rate

Rate zeroYieldImpl(Time) const;

// added (RP, 20100823)

//! returns the spreaded forward rate

Rate forwardImpl(Time) const;

void update();

private:

void updateTimes();

const double calcSpread( Time t ) const;

Handle<YieldTermStructure> originalCurve_;

std::vector<Handle<Quote> > spreads_;

std::vector<Date> dates_;

std::vector<Time> times_;

// added (RP, 2010.08.23)

Compounding comp_;

Frequency freq_;

DayCounter dc_;

};

// inline definitions

inline

PiecewiseZeroSpreadedTermStructure::PiecewiseZeroSpreadedTermStructure(

const Handle<YieldTermStructure>& h,

const std::vector<Handle<Quote> >& spreads,

const std::vector<Date>& dates,

// added (RP, 2010.08.23)

Compounding comp,

Frequency freq,

const DayCounter& dc)

: originalCurve_(h), spreads_(spreads), dates_(dates),

times_(dates_.size()),

// added (RP, 2010.08.23)

comp_(comp), freq_(freq), dc_(dc) {

QL_REQUIRE(!spreads_.empty(), "no spreads given");

QL_REQUIRE(spreads_.size() == dates_.size(),

"spread and date vector have different sizes");

registerWith(originalCurve_);

for (Size i = 0; i < spreads_.size(); i++)

registerWith(spreads_[i]);

updateTimes();

}

inline DayCounter PiecewiseZeroSpreadedTermStructure::dayCounter() const {

return originalCurve_->dayCounter();

}

inline Calendar PiecewiseZeroSpreadedTermStructure::calendar() const {

return originalCurve_->calendar();

}

inline Natural PiecewiseZeroSpreadedTermStructure::settlementDays() const {

return originalCurve_->settlementDays();

}

inline const Date&

PiecewiseZeroSpreadedTermStructure::referenceDate() const {

return originalCurve_->referenceDate();

}

inline Date PiecewiseZeroSpreadedTermStructure::maxDate() const {

return std::min(originalCurve_->maxDate(), dates_.back());

}

inline Rate

PiecewiseZeroSpreadedTermStructure::zeroYieldImpl(Time t) const {

//Rate z = originalCurve_->zeroRate(t, Continuous, NoFrequency, true);

//if (t <= times_.front()) {

// return z + spreads_.front()->value();

//} else if (t >= times_.back()) {

// return z + spreads_.back()->value();

//} else {

// Size i;

// for (i = 0; i < times_.size(); i++)

// if (times_[i] > t) break;

// Time dt = times_[i] - times_[i-1];

// return z + spreads_[i]->value() * (t - times_[i-1]) / dt

// + spreads_[i-1]->value() * (times_[i] - t) / dt;

//}

// added (RP, 20100823)

double spread = calcSpread( t );

InterestRate zeroRate = originalCurve_->zeroRate(t, comp_, freq_, true);

InterestRate spreadedRate(zeroRate + spread,

zeroRate.dayCounter(),

zeroRate.compounding(),

zeroRate.frequency());

return spreadedRate.equivalentRate(Continuous, NoFrequency, t);

}

inline const double

PiecewiseZeroSpreadedTermStructure::calcSpread( Time t ) const {

double spread = 0.0;

if (t <= times_.front()) {

spread = spreads_.front()->value();

} else if (t >= times_.back()) {

spread = spreads_.back()->value();

} else {

Size i;

for (i = 0; i < times_.size(); i++)

if (times_[i] > t) break;

Time dt = times_[i] - times_[i-1];

spread = spreads_[i]->value() * (t - times_[i-1]) / dt

+ spreads_[i-1]->value() * (times_[i] - t) / dt;

}

return spread;

}

inline void PiecewiseZeroSpreadedTermStructure::update() {

updateTimes();

ZeroYieldStructure::update();

}

inline void PiecewiseZeroSpreadedTermStructure::updateTimes() {

for (Size i = 0; i < dates_.size(); i++)

times_[i] = timeFromReference(dates_[i]);

}

}

#endif

50 bps Key Rate Shock (before):

50 bps Key Rate Shock (after fix):

-- Robert Philipp Synapse Financial Engineering 703.623.4063 (mobile) 703.573.0119 (fax) [hidden email] www.synapsefe.com

------------------------------------------------------------------------------

Sell apps to millions through the Intel(R) Atom(Tm) Developer Program

Be part of this innovative community and reach millions of netbook users

worldwide. Take advantage of special opportunities to increase revenue and

speed time-to-market. Join now, and jumpstart your future.

http://p.sf.net/sfu/intel-atom-d2d

_______________________________________________

QuantLib-dev mailing list

[hidden email]

https://lists.sourceforge.net/lists/listinfo/quantlib-dev

| Free forum by Nabble | Edit this page |